Chapter 08. Bitcoin worlds

This is the June 2026 draft of chapter 08 in my new book, When Policy Falls Behind: Bitcoin, AI, and the Governance of Fast Systems. Copyright © 2026 by Murray A Rudd. A pdf version of this chapter is available at: https://dx.doi.org/10.2139/ssrn.6749281

Introduction

Since its conception, Bitcoin (Nakamoto, 2008) has unsettled long-standing assumptions about money, value, and state authority (Böhme et al., 2015; Ba and Şen, 2024). That contestation now runs through institutional finance and public policy: its market capitalization rivals major multinational firms,[1] spot exchange-traded funds channel billions in daily flow,[2] sovereign wealth funds and corporate treasuries hold material allocations,[3] and governments weigh Bitcoin’s role in national economic strategy.[4] Seventeen years of continuous protocol operation have not yet, however, produced settled beliefs about the institutional questions Bitcoin raises (Rudd, 2023).

Federal classification in the USA, state-level treatment, the EU MiCA framework, and Asian regulatory regimes remain isolated and often incompatible (Benson et al., 2024; CFTC and SEC, 2026). US state legislatures pass mining moratoria on environmental grounds in the same political season that the federal executive evaluates Bitcoin as a strategic reserve asset. Developers contest relay policy defaults through informal channels (Chapter 3) because no formal venue exists for adjudicating what the protocol is for (De Filippi and Wright, 2018). Bitcoin has moved from the periphery into disputes over sovereignty, inflation, financial stability, and monetary governance without acquiring a settled institutional environment.

Fiat systems organize monetary elasticity through credit creation, administered interest rates, and lender-of-last-resort facilities (Goodhart, 1988), whereas Bitcoin fixes issuance and lets price absorb shocks (Rudd and Porter, 2025). The collision between absolute scarcity and elastic credit reopens questions about monetary definition, governing authority, stabilization discipline, and the governance forms available when Bitcoin supplies no formal mechanism through which economic stakeholders can register binding preferences (De Filippi and Loveluck, 2016; Notland et al., 2025). Regulatory clarification would not settle that mismatch because the tension manifests in the gap between a monetary architecture that fixes supply and surrounding institutions built to manage stress through credit and discretionary authority.

Advanced economies sharpen that mismatch because fiscal and monetary conditions are themselves unsettled. Persistent primary deficits, rising debt-to-GDP ratios, and political limits on consolidation create fiscal dominance pressure (Sargent and Wallace, 1981; IMF, 2026). Long-run deflationary pressure from technological change and AI-driven productivity gains (Hatzius et al., 2023; Acemoglu, 2025) coexists with near-term inflationary pressure from geopolitical risk, supply-chain shocks, AI infrastructure build-out, and fiscal expansion (Caldara and Iacoviello, 2022; Iacoviello et al., 2024).

Institutional latency appears where that macro setting requires a Bitcoin response that existing governance forms cannot supply quickly or legitimately enough. Bitcoin’s bearer instrument property regime generates bilateral dependencies, Williamson’s (1985) fundamental transformation, that the permissionless architecture was designed to limit (Chapter 5). Those dependencies are governed unevenly across jurisdictions, intermediaries, and epistemic commitments. Prior horizon scanning research identified six cleavages that organize the variation: market depth; policy settlement; custody structure; energy stress; information integrity; and credit leverage exposure (Rudd, 2024, 2025b, 2026). Their combinations produce distinct “Bitcoin worlds,” from reserve-like integration to speculative accelerants and geopolitical hedges.

Morphological scenario analysis (Zwicky, 1967; Ritchey, 2011) gives such variability a structured form. For Bitcoin, I use the approach to enumerate the 64 configurations generated by the six cleavages and classify each as stable or transitional. Governance form analysis (Williamson, 1991) then identifies which transactional attributes support each configuration and which erode it. Resilience profiles show which configurations can absorb specific threat classes and which move toward institutional latency when the required governance form is unavailable.

Bitcoin worlds are configurations rather than specific forecasts. Structural settings determine which configurations are coherent, which are transitional, and which threat classes each can absorb. Epistemic commitments then determine which coherent configurations are admissible. A configuration can be operationally durable and still surrender the properties that make Bitcoin institutionally distinctive.

Sovereignty-first commitments illustrate that distinction. A commitment to Bitcoin’s bearer instrument property and permissionless protocol access rules out configurations dependent on concentrated custody and credit leverage even where those configurations are operationally coherent. Bitcoin can function as a monetary asset (Narayanan et al., 2016) and as an institutional commitment device (Chapter 7). Configurations that preserve or erode its commitment properties therefore carry consequences beyond private return, custody preference, or monetary-sovereignty claims: they affect the supply of temporal infrastructure available for long-horizon deliberation and lower time preferences.

The contest over Bitcoin’s institutional future has, I believe, been posed in the wrong terms, conducted as though operational stability would settle it, when stability and institutional meaning are separate questions. The configuration space holds the two apart and I use it to establish where they diverge: where financialization selects configurations that are durable yet strip Bitcoin of the commitment properties sovereignty-first holders refuse to surrender. That divergence falls on the region in which Bitcoin’s anchor stock function is preserved or lost, which is why the stakes are temporal rather than being confined only to private risk and return. I argue that Bitcoin’s institutional trajectory can no longer be read off stability alone; it must be read off the commitments the surrounding environment is willing to sustain against the momentum that erodes them.

Cleavages of the Bitcoin institutional space

Bitcoin communities hold divergent priors on Bitcoin scarcity, governance form and hierarchy, and purpose (De Filippi and Loveluck, 2016; Hayes, 2019; Humayun, 2019; Rudd, 2024, 2025a, 2026), while surrounding legal, financial, and energy systems remain fragmented across jurisdictions (Benson et al., 2024). Morphological scenario analysis fits that setting because the problem is configurational (Zwicky, 1967; Ritchey, 2011): the institutional role that Bitcoin takes on depends critically on how structural drivers combine rather than on any single variable moving alone.

The six binary cleavages in Table 8.1 keep that configuration problem tractable. They identify the main axes along which Bitcoin’s institutional role changes (Rudd, 2025b): liquidity depth, L; policy clarity, P; concentration of holdings, C; macro-energy stress, E; trust and information integrity, T; and credit leverage, V. Binary coding simplifies continuous conditions, yet it also makes the interaction among the cleavages visible enough to test.

| Cleavage | Coding (1 / 0) | Operational definition | Institutional grounding |

|---|---|---|---|

| Liquidity depth (L) | Deep / thin | Order book depth cushions volatility; thin markets magnify shocks. Routine flows from ETF creations, miner payouts, and corporate treasury rebalancing are either absorbed or propagated as volatility | Bitcoin’s anchor stock function is slow-moving while the information environment it trades in turns over quickly; that asymmetry leaves liquidity to absorb the mismatch, so depth is continuously pressured rather than settling at a stable level |

| Policy clarity (P) | Supportive / hostile | Harmonized supportive rules lower compliance costs and stabilize institutional access. Hostile or fragmented regimes scatter flows into thin or opaque venues | Williamsonian governance forms required to manage bearer instrument property regimes fragment along jurisdictional and doctrinal lines |

| Concentration (C) | Concentrated / diffuse | Concentrated custodianship supplies institutional convenience while amplifying single point fragility. Diffusion preserves exit optionality at the holder level | The fundamental transformation operating at the custody interface concentrates governance leverage in custodians whose bilateral dependencies with their clients lock both parties into configurations that the permissionless Bitcoin architecture was designed to prevent |

| Macro and energy stress (E) | High / low | Production costs are dominated by electricity, making the protocol vulnerable to energy price spikes and grid strain. Macroeconomic stress amplifies energy market disruption and political pressure on mining operations | The value filter through which Bitcoin mining claims become operational rules operates differently across scales and macro conditions, with stress regimes determining whether claims are filtered or contested |

| Trust and information integrity (T) | Trustworthy / unreliable | Continuous proof of reserves, transparent custody, and verifiable flows anchor confidence. Opacity widens spreads and destabilizes pricing | Attestation infrastructure operates at epistemic layer where rule-making authority is determined, shaping lower-level decisions about how assets are held through intermediaries outside the consensus mechanism |

| Credit leverage (V) | High / low | Credit-funded exposure, derivatives, lending, and margin structures either amplify price movements through forced adjustment or leave price discovery to unlevered spot-market transmission. | Leverage transforms Bitcoin’s profile by increasing uncertainty, exit costs, and crisis-response frequency. In Williamsonian terms, it pushes configurations toward relational or hierarchical governance requirements that Bitcoin’s architecture does not itself supply |

Table 8.1. Six cleavages of the Bitcoin institutional space

The cleavages are structural variables rather than neutral descriptors. Concentrated custody can operate as institutional access infrastructure or as single-point governance fragility, while credit leverage can deepen liquidity and price discovery or compress Bitcoin’s commitment properties into short-horizon credit dynamics. Binary coding trades resolution for tractability (intermediate states are common) and where those states matter for stability assessment, I flag the dependency rather than refine the coding.

Three criteria discipline the selection. A cleavage must: cut across the institutional analysis rather than belong to one strand; operate across Bitcoin’s operational, implementation, political, and epistemic levels, and correspond to a lever that policymakers, market participants, or institutional actors can plausibly move. Those criteria keep the space non-redundant because co-movement is partial and the six-dimensional structure remains analytically real.

The framework was tested against a consolidated dataset of horizon-scan issues drawn from Bitcoin discourse across 2023, 2024, and 2025, comprising 57,870 individual issues from 5,787 long-form podcast episodes. The six cleavages directly capture 54% of issues, with another 18% covered by adjacent themes (Appendix A), and the temporal pattern is consistent with the institutional claim: V grows from 2.2% of issues in 2023 to 7.9% in 2025; P, C, and L rise in the post-ETF environment; E falls modestly while remaining the single most-mentioned cleavage. The discourse shifted somewhat over time as energy-dominated concerns gave way toward financial architecture concerns.

Reading the configuration space

Each configuration in Table 8.2 carries a six-digit binary code in the order L P C E T V. A digit is 1 when the cleavage takes its first value: deep liquidity; supportive policy; concentrated holdings; macro-energy stress; credible attestation; or high credit leverage. It is 0 when the cleavage takes the opposite value. Configuration 110010, for example, denotes deep liquidity, supportive policy, diffuse holdings, benign macro conditions, credible attestation, and low leverage (labeled “Clear Open Reserve”). The ordering follows the binary enumeration produced by the six cleavages, grouping configurations by shared structural features rather than by stability or analytical priority.

Eight archetypes name the base configurations produced by L, P, and C: Wildcat Frontier; Citadel Frontier; Open Frontier; Walled Frontier; Diffuse Siege; Custodial Siege; Open Reserve; and Custodian Hub. These three cleavages define the configuration’s institutional structure, market depth, policy alignment, and holding distribution. E, T, and V then operate as modifiers, changing exposure conditions without changing the underlying structural position.

The labels are deliberately mixed in tone. Custodian Hub and Open Reserve evoke institutional consolidation, Custodial Siege and Diffuse Siege evoke contestation, and Wildcat Frontier, Open Frontier, Walled Frontier, and Citadel Frontier evoke unsettled or early-stage conditions. No archetype is the natural center of the space. Each names a region that contemporary Bitcoin discourse can credibly occupy, while each modifier combination identifies a variant that institutional dynamics can plausibly produce.

Every configuration in the matrix has a counterpart differing in any single cleavage. For example, configuration 1, Citadel Frontier, and configuration 2, Citadel Frontier Levered, differ only in V, allowing the effect of leverage to be read while the other five cleavages are held constant. Archetype blocks show how one institutional structure performs under stress or benign conditions, credible or weak attestation, and leverage or no leverage. Durability is not determined by structural foundation alone.

Configurations also differ in institutional distance. Two configurations separated by one cleavage are adjacent; configurations separated by three or four cleavages are distant. Movement through the space would usually occur through single-cleavage transitions: regulatory change moves P, market deepening moves L, credible attestation reform moves T, and credit expansion moves V. The configuration space therefore identifies stable worlds and the transitions that institutional change makes more readily available.

| # | Code L P C E T V |

Title | Snapshot | Stable |

|---|---|---|---|---|

| 1 | 001000 | Citadel Frontier | Thin liquidity, hostile policy, concentrated holdings, and weak information integrity remain stable because unlevered exposure gives shocks no credit channel to amplify through. | Yes |

| 2 | 001001 | Citadel Frontier Levered | Leverage enters a thin, hostile, concentrated, opaque market with no policy backstop or liquidity buffer, leaving the first credit cycle to force disorderly liquidation. | No |

| 3 | 001010 | Clear Citadel Frontier | Thin liquidity and hostile policy coexist with concentrated holdings and credible attestations; absent leverage, transparency does not create a destabilizing transmission channel. | Yes |

| 4 | 001011 | Clear Citadel Frontier Levered | Transparent leverage in a thin, hostile, concentrated market turns drawdowns into visible margin pressure, making cascade dynamics dominate any institutional support. | No |

| 5 | 001100 | Stressed Citadel Frontier | Macro-energy stress strains thin, hostile, concentrated, opaque markets while unlevered exposure confines the pressure to operating margins and holder adjustment. | Yes |

| 6 | 001101 | Stressed Citadel Frontier Levered | Leverage, thin liquidity, hostile policy, concentration, opacity, and macro-energy stress combine without absorption capacity, exhausting private risk management before the cycle resolves. | No |

| 7 | 001110 | Stressed Clear Citadel Frontier | Credible attestations make positions legible in a thin, hostile, concentrated, stressed market while the absence of leverage prevents stress from becoming a credit cascade. | Yes |

| 8 | 001111 | Stressed Clear Citadel Frontier Levered | Transparent leverage in a thin, hostile, concentrated, stressed market exposes positions to immediate mark-to-market pressure and forces destabilizing liquidation. | No |

| 9 | 000000 | Wildcat Frontier | Thin liquidity, hostile policy, diffuse holdings, and weak information integrity remain stable because unlevered exposure leaves shocks to dissipate through holder behavior. | Yes |

| 10 | 000001 | Wildcat Frontier Levered | Leverage enters a thin, hostile, diffuse, opaque market with no policy backstop or liquidity buffer, leaving liquidation pressure without institutional absorption. | No |

| 11 | 000010 | Clear Wildcat Frontier | Thin liquidity and hostile policy coexist with diffuse holdings and credible attestations; absent leverage, transparency does not create a destabilizing transmission channel. | Yes |

| 12 | 000011 | Clear Wildcat Frontier Levered | Transparent leverage in a thin, hostile, diffuse market turns drawdowns into visible margin pressure and makes deleveraging the dominant transmission mechanism. | No |

| 13 | 000100 | Stressed Wildcat Frontier | Macro-energy stress strains thin, hostile, diffuse, opaque markets while unlevered exposure confines adjustment to operating margins and holder behavior. | Yes |

| 14 | 000101 | Stressed Wildcat Frontier Levered | Thin liquidity, hostile policy, diffuse holdings, opacity, leverage, and macro-energy stress combine without a buffering institution or market depth to absorb the cycle. | No |

| 15 | 000110 | Stressed Clear Wildcat Frontier | Credible attestations make positions legible in a thin, hostile, diffuse, stressed market while the absence of leverage prevents a credit-amplified cascade. | Yes |

| 16 | 000111 | Stressed Clear Wildcat Frontier Levered | Transparent leverage in a thin, hostile, diffuse, stressed market exposes positions to immediate mark-to-market pressure and forces destabilizing liquidation. | No |

| 17 | 011000 | Walled Frontier | Supportive policy stabilizes thin, concentrated, opaque markets; without leverage, ordinary shocks remain contained by holder behavior and intermediary buffering. | Yes |

| 18 | 011001 | Walled Frontier Levered | Opaque leverage in a thin but supportive and concentrated market produces recurrent squeeze-and-release dynamics that policy tolerance and intermediary balance sheets contain. | Yes |

| 19 | 011010 | Clear Walled Frontier | Supportive policy and credible attestations stabilize thin, concentrated markets; absent leverage, transparency improves legibility without creating cascade pressure. | Yes |

| 20 | 011011 | Clear Walled Frontier Levered | Transparent leverage in a thin, supportive, concentrated market makes visible margin pressure dominate, overwhelming the stabilizing effects of policy support. | No |

| 21 | 011100 | Stressed Walled Frontier | Supportive policy stabilizes thin, concentrated, opaque markets under macro-energy stress because no leverage channel amplifies operating pressure into systemic liquidation. | Yes |

| 22 | 011101 | Stressed Walled Frontier Levered | Opaque leverage in a thin, supportive, concentrated, stressed market remains stable while regulatory tolerance and intermediary balance sheets absorb squeeze-and-release cycles. | Yes |

| 23 | 011110 | Stressed Clear Walled Frontier | Supportive policy and credible attestations stabilize thin, concentrated markets under macro-energy stress; absent leverage, stress does not propagate through credit. | Yes |

| 24 | 011111 | Stressed Clear Walled Frontier Levered | Transparent leverage in a thin, supportive, concentrated, stressed market turns drawdowns into visible margin pressure that policy support cannot neutralize. | No |

| 25 | 010000 | Open Frontier | Supportive policy stabilizes thin, diffuse, opaque markets; without leverage, shocks remain local rather than becoming system-wide credit events. | Yes |

| 26 | 010001 | Open Frontier Levered | Opaque leverage in a thin but supportive and diffuse market produces recurrent squeeze-and-release dynamics contained by policy tolerance and intermediary buffering. | Yes |

| 27 | 010010 | Clear Open Frontier | Supportive policy and credible attestations stabilize thin, diffuse markets; absent leverage, transparency improves legibility without triggering forced adjustment. | Yes |

| 28 | 010011 | Clear Open Frontier Levered | Transparent leverage in a thin, supportive, diffuse market converts drawdowns into visible margin pressure and makes deleveraging dominate the configuration. | No |

| 29 | 010100 | Stressed Open Frontier | Supportive policy stabilizes thin, diffuse, opaque markets under macro-energy stress because no leverage channel amplifies operating pressure into systemic liquidation. | Yes |

| 30 | 010101 | Stressed Open Frontier Levered | Opaque leverage in a thin, supportive, diffuse, stressed market remains stable while regulatory tolerance and intermediary buffering absorb credit-cycle pressure. | Yes |

| 31 | 010110 | Stressed Clear Open Frontier | Supportive policy and credible attestations stabilize thin, diffuse markets under macro-energy stress; absent leverage, stress does not propagate through credit. | Yes |

| 32 | 010111 | Stressed Clear Open Frontier Levered | Transparent leverage in a thin, supportive, diffuse, stressed market turns drawdowns into visible margin pressure that policy support cannot neutralize. | No |

| 33 | 101000 | Custodial Siege | Deep liquidity stabilizes hostile, concentrated, opaque markets; without leverage, ordinary shocks are absorbed by market depth and intermediary buffering. | Yes |

| 34 | 101001 | Custodial Siege Levered | Opaque leverage in a deep, hostile, concentrated market remains stable while market depth and private risk management absorb episodic credit cycles. | Yes |

| 35 | 101010 | Clear Custodial Siege | Deep liquidity cannot offset hostile policy when concentrated custody and credible attestations make intermediary positions legible and exit options narrow. | No |

| 36 | 101011 | Clear Custodial Siege Levered | Transparent leverage in a deep, hostile, concentrated market exposes positions to mark-to-market pressure; depth cannot stop disclosure-driven deleveraging. | No |

| 37 | 101100 | Stressed Custodial Siege | Deep liquidity stabilizes hostile, concentrated, opaque markets under macro-energy stress because unlevered exposure prevents stress from becoming a credit cascade. | Yes |

| 38 | 101101 | Stressed Custodial Siege Levered | Opaque leverage in a deep, hostile, concentrated, stressed market fails when policy hostility and macro-energy stress exhaust intermediary buffering capacity. | No |

| 39 | 101110 | Stressed Clear Custodial Siege | Hostile policy, concentrated custody, credible attestations, and macro-energy stress make transparent intermediaries brittle despite deep liquidity. | No |

| 40 | 101111 | Stressed Clear Custodial Siege Levered | Transparent leverage in a deep, hostile, concentrated, stressed market makes disclosure-driven margin pressure dominate market-depth absorption. | No |

| 41 | 100000 | Diffuse Siege | Deep liquidity stabilizes hostile, diffuse, opaque markets; without leverage, ordinary shocks are absorbed by market depth and holder adjustment. | Yes |

| 42 | 100001 | Diffuse Siege Levered | Opaque leverage in a deep, hostile, diffuse market remains stable while market depth and private risk management absorb episodic credit cycles. | Yes |

| 43 | 100010 | Clear Diffuse Siege | Deep liquidity and diffuse holdings stabilize hostile markets with credible attestations; absent leverage, transparency does not create cascade pressure. | Yes |

| 44 | 100011 | Clear Diffuse Siege Levered | Transparent leverage in a deep, hostile, diffuse market exposes positions to mark-to-market pressure; depth cannot stop disclosure-driven deleveraging. | No |

| 45 | 100100 | Stressed Diffuse Siege | Deep liquidity stabilizes hostile, diffuse, opaque markets under macro-energy stress because unlevered exposure prevents stress from becoming a credit cascade. | Yes |

| 46 | 100101 | Stressed Diffuse Siege Levered | Opaque leverage in a deep, hostile, diffuse, stressed market fails when policy hostility and macro-energy stress exhaust intermediary buffering capacity. | No |

| 47 | 100110 | Stressed Clear Diffuse Siege | Deep liquidity, diffuse holdings, and credible attestations stabilize hostile markets under macro-energy stress because no leverage channel amplifies the shock. | Yes |

| 48 | 100111 | Stressed Clear Diffuse Siege Levered | Transparent leverage in a deep, hostile, diffuse, stressed market makes disclosure-driven margin pressure dominate market-depth absorption. | No |

| 49 | 111000 | Custodian Hub | Deep liquidity and supportive policy stabilize concentrated, opaque holdings; without leverage, ordinary shocks remain absorbed by market depth and intermediaries. | Yes |

| 50 | 111001 | Custodian Hub Levered | Opaque leverage in a deep, supportive, concentrated market remains stable while market depth, policy support, and intermediary balance sheets absorb credit cycles. | Yes |

| 51 | 111010 | Clear Custodian Hub | Deep liquidity, supportive policy, concentrated holdings, and credible attestations remain stable because unlevered transparency has no credit channel to transmit through. | Yes |

| 52 | 111011 | Clear Custodian Hub Levered | Transparent leverage in a deep, supportive, concentrated market exposes positions to margin pressure; institutional support cannot neutralize disclosure-driven cascade dynamics. | No |

| 53 | 111100 | Stressed Custodian Hub | Deep liquidity and supportive policy stabilize concentrated, opaque holdings under macro-energy stress because no leverage channel amplifies the shock. | Yes |

| 54 | 111101 | Stressed Custodian Hub Levered | Opaque leverage in a deep, supportive, concentrated, stressed market remains stable while depth, policy support, and intermediaries absorb credit-cycle pressure. | Yes |

| 55 | 111110 | Stressed Clear Custodian Hub | Deep liquidity, supportive policy, concentrated holdings, and credible attestations remain stable under macro-energy stress because no leverage channel amplifies the shock. | Yes |

| 56 | 111111 | Stressed Clear Custodian Hub Levered | Transparent leverage in a deep, supportive, concentrated, stressed market makes disclosure-driven margin pressure dominate market-depth and policy absorption. | No |

| 57 | 110000 | Open Reserve | Deep liquidity and supportive policy stabilize diffuse, opaque holdings; without leverage, ordinary shocks remain absorbed by market depth and holder adjustment. | Yes |

| 58 | 110001 | Open Reserve Levered | Opaque leverage in a deep, supportive, diffuse market remains stable while market depth, policy support, and intermediary balance sheets absorb credit cycles. | Yes |

| 59 | 110010 | Clear Open Reserve | Deep liquidity, supportive policy, diffuse holdings, and credible attestations remain stable because unlevered transparency has no credit channel to transmit through. | Yes |

| 60 | 110011 | Clear Open Reserve Levered | Transparent leverage in a deep, supportive, diffuse market exposes positions to margin pressure; institutional support cannot neutralize disclosure-driven cascade dynamics. | No |

| 61 | 110100 | Stressed Open Reserve | Deep liquidity and supportive policy stabilize diffuse, opaque holdings under macro-energy stress because no leverage channel amplifies the shock. | Yes |

| 62 | 110101 | Stressed Open Reserve Levered | Opaque leverage in a deep, supportive, diffuse, stressed market remains stable while depth, policy support, and intermediaries absorb credit-cycle pressure. | Yes |

| 63 | 110110 | Stressed Clear Open Reserve | Deep liquidity, supportive policy, diffuse holdings, and credible attestations remain stable under macro-energy stress because no leverage channel amplifies the shock. | Yes |

| 64 | 110111 | Stressed Clear Open Reserve Levered | Transparent leverage in a deep, supportive, diffuse, stressed market makes disclosure-driven margin pressure dominate market-depth and policy absorption. | No |

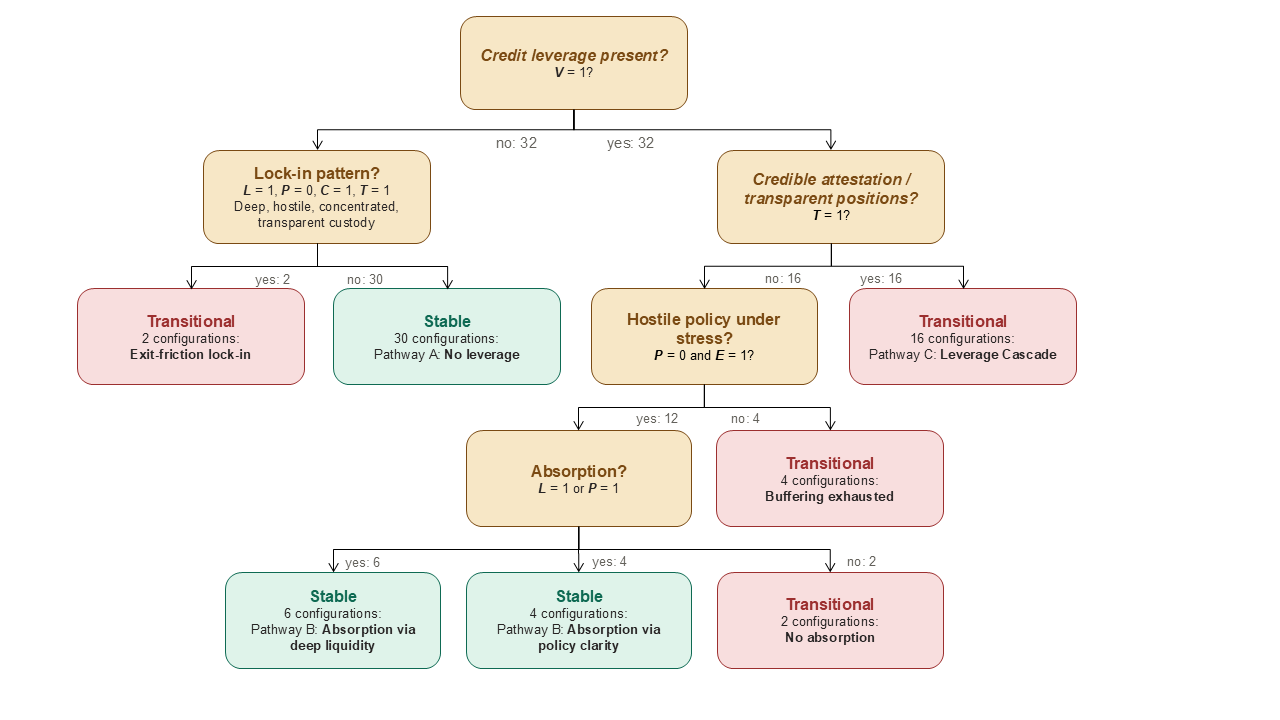

The stability decision tree

Leverage as the first split

Forty of the 64 configurations are stable and 24 are transitional. Figure 8.1 shows the decision pathway behind that distribution, with credit leverage tested first because it is the strongest determinant of stability: the split produces a 22-configuration swing between V = 0, where 30 of 32 configurations are stable, and V = 1, where 10 of 32 are stable. T is tested next on the leveraged branch because transparency changes how leverage propagates. The remaining cleavages enter only where leverage and transparency leave the outcome unresolved.

Configurations without leverage are stable across 30 cells, with two exceptions where deep liquidity, hostile policy, concentrated holdings, and credible attestation combine in a lock-in pattern (configurations 35 and 39). Transparent intermediary positions become legible to hostile authorities while concentration removes the diffuse exit options that would otherwise relieve pressure. Macro-energy stress in configuration 39 accelerates deterioration without changing the mechanism. Lock-in is a specific failure mode of architecturally consolidated, unlevered configurations under hostile policy, not a general vulnerability of unlevered Bitcoin exposure.

Leveraged configurations with credible attestation are transitional across all 16 cells. Continuous mark-to-market valuation converts price drawdowns into margin calls regardless of market depth, policy support, concentration, or stress conditions. Deep markets do not absorb the cascade because the cascade operates through disclosure itself. Supportive policy does not contain it because the policy apparatus reinforces the legibility infrastructure through which the unwind occurs. Transparency stabilizes unlevered settings and becomes the channel through which credit cycles propagate when leverage is present.

Transparency is not intrinsically destabilizing [34]. In conventional financial systems, transparent leveraged exposure can be stabilizing when paired with central clearing, coordinated supervision, discretionary liquidity provision, and credible crisis resolution authority [9, 35]. The failure mode isolated here is leveraged Bitcoin exposure whose attestation infrastructure makes positions legible without supplying a governance form able to slow or absorb forced adjustment. Under those conditions, transparency changes from a monitoring device into a synchronization device: it reveals the positions that must be adjusted, aligns expectations around that adjustment, and compresses the time available for balance-sheet absorption. The instability originates in the conjunction of leverage, legibility, and insufficient governance response capacity.

Figure 8.1. Stability decision tree for the 64-world matrix

Opaque leverage has a different failure boundary. When hostile policy combines with macro-energy stress, intermediary buffering fails before the credit cycle resolves because hostile policy raises the cost of balance sheet expansion while stress raises the cost of holding through drawdowns. Four configurations are transitional at this level. Where that compound pressure is absent, opaque leverage is stable when absorption capacity exists: deep liquidity supplies absorption directly in six configurations, and supportive policy supplies it indirectly in four more by anchoring expectations of orderly intervention. Two configurations remain transitional because thin markets under hostile policy provide neither absorption channel.

Three stability pathways

Three pathways account for 56 of the 64 configurations. Pathway A, the V = 0 branch outside the lock-in pattern, contains 30 stable configurations and rests on the absence of credit leverage transmission. Pathway B, opaque leverage with absorption capacity, contains 10 stable configurations and rests on intermediary internalization as a different governance form from transparent risk distribution. Pathway C, transparent leverage, contains 16 transitional configurations and identifies mark-to-market discipline as the dominant transmission mechanism. The remaining eight configurations are narrower exceptions: two lock-in cases, four buffering-exhausted cases, and two no-absorption cases.

The pathways differ because each rests on a different institutional mechanism. Pathway A is stable because no credit channel turns structural variation into systemic instability. Pathway B is stable because opaque intermediation substitutes balance sheet absorption for transparent risk distribution, provided the supporting structure holds. Pathway C is transitional because transparency converts leverage cycles into imminent deleveraging cascades while no other cleavage neutralizes the trigger. These are different governance problems occupying different regions of the configuration space, not symmetric variants of one logic.

Transparency, cascade, and lock-in

The transparency-leverage interaction inverts the usual reading of transparency as a stabilizing feature. Transparency reduces information asymmetry (Akerlof, 1970) and supports orderly markets where leverage is absent, while the same legibility accelerates the resolution of credit stress when leverage is present (Brunnermeier et al., 2009; Geanakoplos, 2010). Under high-amplitude credit dynamics, accelerated resolution produces cascade rather than soft landing. Opacity routes the same cycles through intermediary balance sheets that price the opacity and contain stress within capital buffers (Dang et al., 2017). That arrangement is not normatively preferable; it has a different operational property.

Two structural asymmetries follow. V = 1 and T = 1 is the only two-cleavage conjunction that determines the outcome regardless of the other four cleavages, because the supporting features either fail to neutralize the cascade mechanism or, in the case of supportive policy and credible attestation, reinforce the legibility through which it operates. The lock-in pattern is more demanding because it requires L = 1, P = 0, C = 1, and T = 1. Configurations 35 and 39 are the only V = 0 transitional cases, so lock-in is analytically rare rather than representative of unlevered configurations.

Governance form typing and resilience

Governance via markets, hierarchies, and hybrids

The three pathways through the decision tree map onto governance forms – markets, hierarchies, or hybrid forms that minimize transaction costs (Williamson, 1991) – through the transactional attributes each pathway carries. Pathway A, where V is absent, suggests governance through markets minimizes transaction costs. Holding decisions are low frequency, exit remains available, and the asset’s transactional profile does not require relationship-specific intermediation. Holders carry residual uncertainty individually; intermediaries provide execution rather than risk internalization; and coordination occurs through price rather than bilateral governance. The 30 stable configurations on this pathway are cases in which market form is institutionally available and adequate to the transaction.

Pathway B requires a hybrid form because leverage is present, credible attestation is absent, and absorption capacity exists. Opaque intermediaries internalize the credit risk that leverage introduces, supplying balance-sheet capacity, private risk management, and reputation-based commitment. Stability depends on whether the surrounding structure can support that hybrid form: deep markets supply trading depth for absorption, while supportive policy supplies the regulatory setting that anchors expectations of orderly intervention. Where one support is present, ten configurations sustain hybrid form; where neither is present, credit cycles arrive without an institutional buffer and the configuration becomes transitional.

Pathway C would require a hierarchical form to govern the credit dynamics that transparent leverage generates. Transparent leveraged exposure at scale can be stable where central clearing, coordinated supervision, crisis-liquidity capacity, and loss-allocation authority exist (Brunnermeier et al., 2009; Duffie and Zhu, 2011). Bitcoin’s architecture supplies none of these at the protocol level (Narayanan et al., 2016). The protocol has no central counterparty by design, no lender of last resort exists for an asset whose monetary properties depend on absolute scarcity, and supervisory authority remains jurisdictional while cascade dynamics operate across venues and at the speed of margin calls. Pathway C is transitional because attestation supplies legibility without the hierarchy-relevant capacities needed to slow, absorb, or coordinate forced adjustment.

Resilience implications

Governance form typing gives the stability results a resilience interpretation. The modifier cleavages introduce three threat classes – macro-energy stress, hostile policy, and credit leverage – and the relevant question is whether the supporting governance form can absorb those threats without reorganizing. Pathway A configurations are resilient under stress and policy hostility because the market-oriented governance form for unlevered holding does not depend on supportive policy and is largely indifferent to macro conditions. The two lock-in configurations are exceptions because deep liquidity, concentrated custody, and transparency under hostile policy create relationship-specific commitments that the policy environment converts into liability.

Pathway B configurations are resilient under most threat classes because a hybrid governance form can absorb credit cycles through intermediary balance sheet capacity. The four buffering-exhausted configurations show where hybrid form fails: hostile policy raises the cost of balance sheet expansion while macro-energy stress raises the cost of holding through drawdowns. The supporting structure cannot sustain both pressures simultaneously. The two no-absorption configurations show where hybrid form cannot be sustained at all because thin markets and hostile policy provide neither deep liquidity nor policy support.

Pathway C configurations are not resilient because the governance form they require is institutionally unavailable. The cascade is not a stress response that some configurations weather and others do not; it is the consequence of governance form requirements exceeding governance form availability. Lock-in, exhausted buffering capacity, and lack of absorption are governance strain-oriented failures, while leverage cascade is a governance form failure.

The algorithmic velocity to institutional latency relationship (Chapter 2) gives these resilience claims their temporal structure. Bitcoin’s protocol execution is constant across the configuration space because transactions settle at network speed regardless of surrounding cleavage values. Informational turnover varies by configuration. Where leverage is absent, the relevant informational substrate turns over at a pace with which decision-making can plausibly keep pace. Where leverage is present, position information turns over at roughly the pace margin systems require. Credible attestation under leverage pushes that turnover into mark-to-market timeframes, while opacity routes the same dynamics through intermediary balance sheets that buffer informational turnover within slower capital structures.

Institutional latency is the friction between those temporal profiles and governance response capacity. Where a configuration’s governance form can absorb its informational turnover, institutional response remains slower than protocol execution but remains fast enough for the deliberation that the governance form requires. Where the governance form cannot absorb informational turnover, institutional latency becomes acute, with the cascade case as the limiting example.

The stability assessments are thus also institutional latency assessments. Stable configurations are those in which velocity profile and governance form are mutually compatible, while transitional configurations are those in which they are not. A configuration can show low latency under threats its governance form is built to absorb and high latency under threats that require the form to reorganize.

Sovereignty-first and stability-first as governance form predictions

Two orientations

Two orientations organize contested predictions about Bitcoin’s institutional trajectory. Stability-first, consistent with New Institutional Economics (North, 1990; Coase, 1992; Williamson, 2000) and Keynesian and post-Keynesian traditions (Keynes, 1930; Minsky, 1986; Lavoie, 2014), expects Bitcoin’s transactional attributes to support institutional consolidation through hierarchy and hybrid forms: concentrated custody; credible attestation; supportive policy; and the regulatory apparatus orderly markets require. Sovereignty-first, aligned more with Ostromian polycentric governance (Ostrom, 1990; Ostrom, 1997; Ostrom, 2010), the Old Institutional Economics (Veblen, 1898; Hodgson, 1998), and the Austrian tradition (Rothbard, 1977; Von Hayek, 2009; Boettke et al., 2016), expects the same attributes to favor exit-oriented practices: diffuse self-custody; limited dependence on attestation infrastructure; and resilience under hostile or absent policy.

Neither prediction receives symmetric support. Stability-first’s canonical region, concentrated holdings combined with credible institutional attestation, contains six stable configurations out of sixteen. Ten fail through cascade when leverage is present or through lock-in when policy turns hostile. Sovereignty-first’s canonical region, diffuse holdings combined with credible attestation, contains eight stable configurations out of 16; the eight failures all occur on Pathway C, where leverage and credible attestation interact to force cascade dynamics. The difference is real but smaller than a simple count comparison suggests because both orientations are vulnerable when leverage creates governance form requirements the surrounding institutional environment cannot satisfy.

Hybrid configurations carry more weight than canonical ones. Stability-leaning hybrids, with concentrated holdings and weak institutional attestation, are stable in thirteen of sixteen cases, and sovereignty-leaning hybrids, with diffuse holdings and weak institutional attestation, are also stable in thirteen of sixteen cases. Both avoid Pathway C by construction because T = 0, and the cascade requires V = 1 and T = 1. Twenty-six of 40 stable configurations occupy this hybrid space, so operational durability sits most reliably in configurations neither orientation treats as canonical.

The result appears paradoxical only if operational durability and institutional legitimacy are treated as the same criterion. Stability-first treats opacity as inadequate institutional development. Sovereignty-first is largely indifferent to institutional attestation, while valuing the protocol-level verifiability that makes self-custody meaningful. The most durable cells are configurations where institutional attestation is weak and concentration may be present or absent. The structural assessment identifies a contested middle in which neither orientation’s canonical form holds privileged operational ground.

Pathway C concentrates the vulnerability shared across orientations. All 16 Pathway C configurations have V = 1 and T = 1, divided evenly between the canonical stability-first and sovereignty-first regions. The cascade does not respect the normative axis: from the stability-first reading, it is a failure of supporting institutional infrastructure because hierarchical governance is required but unavailable (see Chapter 3); from the sovereignty-first reading, it is the predictable consequence of attaching credit leverage to an architecture designed to resist governance forms incompatible with Bitcoin’s bearer instrument property. The readings differ in which side of the mismatch they treat as the problem to be solved.

Trajectory asymmetry

Hirschman’s (1970) voice versus exit framework helps clarify the divergence. Stability-first privileges voice mechanisms that Bitcoin’s architecture does not formally supply, while sovereignty-first privileges exit mechanisms that the architecture supplies by design. Stress and policy hostility therefore threaten stability-first configurations by degrading the supporting infrastructure they require, while sovereignty-first configurations absorb those threats more readily when exit options remain available. Leverage operates against both orientations by generating governance form requirements neither can fully satisfy from within its canonical commitments.

Structural symmetry in the configuration space does not imply trajectory symmetry in the world. The custody interface creates a path-dependent bias toward financialization independent of which configurations appear more durable (Chapter 5). Compliance investments, regulatory frameworks, fiduciary precedent, ETF wrappers, and custodial intermediation generate increasing returns that progressively narrow the set of feasible alternatives. Sovereignty-first arrangements lack comparable institutional momentum because exit options do not, by themselves, generate the infrastructure that path-dependent processes require. A structurally fragile leveraged trajectory can therefore remain empirically powerful.

Two conditional counterweights operate against financialization. The gateway dynamic identifies individual-level migration through which some holders who enter Bitcoin through institutional custody move toward self-custody as their relationship with the asset develops (see Chapter 5). Structural unwinding identifies an exogenous shift in which degradation of the monetary, legal, regulatory, or financial conditions supporting custodial arrangements changes the cost-benefit calculus independent of holder preference. Sovereignty-first is therefore both an existing epistemic commitment and a resilience response under structural unwinding. Its commitments predate financialization, although the conditions under which they regain institutional advantage may be produced by the weakening of financialization’s supporting structures.

Epistemic admissibility

So far, the structural analysis takes the configuration space as given and assesses operational stability across it. The orientations, however, operate at the epistemic level (see Chapter 3). They are commitments about what Bitcoin is for (Maurer et al., 2013; Swartz, 2018; Nabben, 2023) and they determine which configurations are eligible for sustained institutional investment before any stability assessment begins. The two orientations differ in the operation their values perform on the shared space.

Stability-first commitments do not narrow the configuration space. Profitability, firm-level returns, transaction cost minimization, and integration with existing financial infrastructure rank configurations rather than exclude them. The full 64-configuration space remains eligible for institutional investment under stability-first, with the orientation selecting within it using the economic criteria the institutional environment supplies.

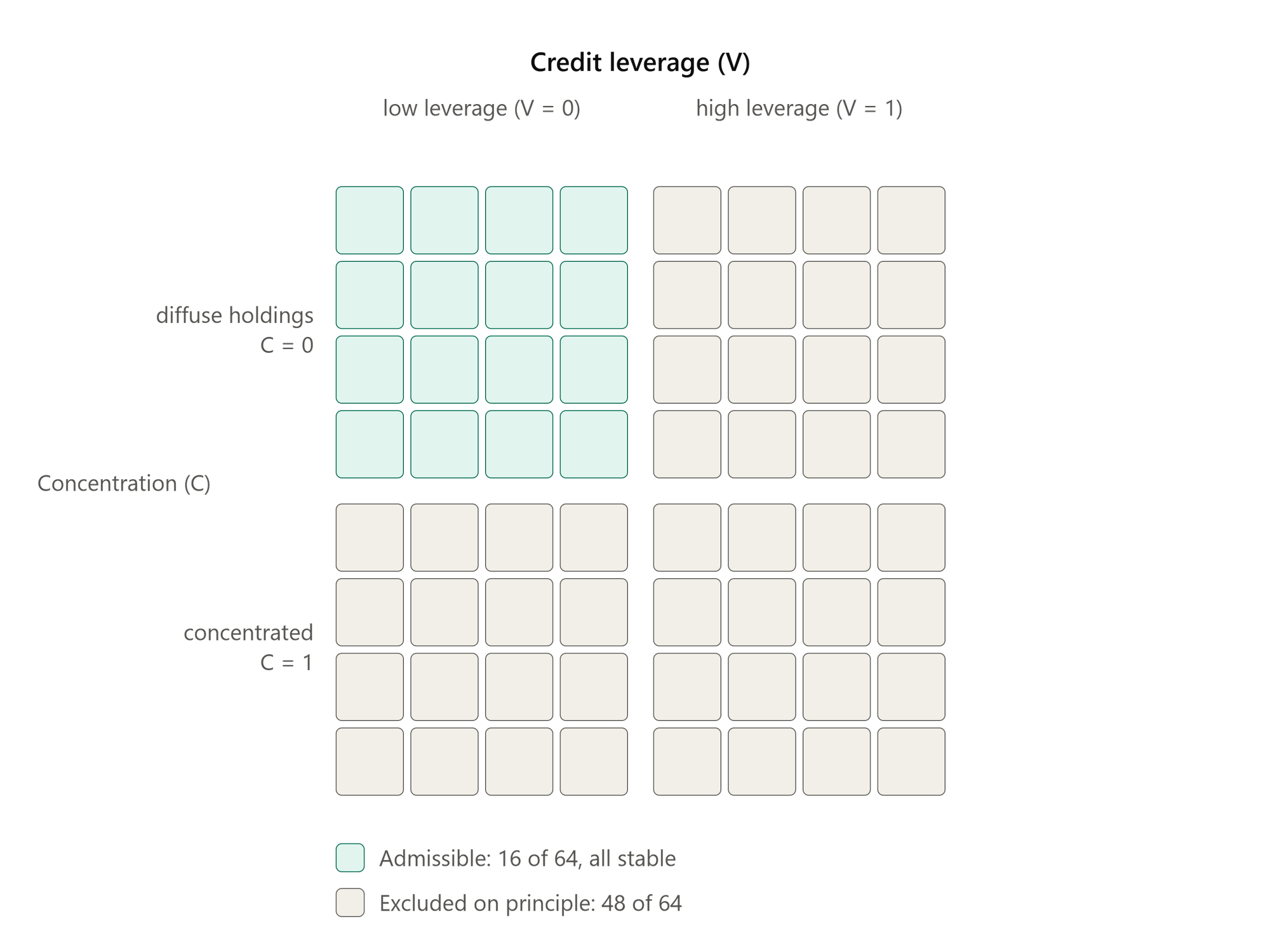

Sovereignty-first commitments narrow the configuration space by taking specific configurations off the table on principle. Bitcoin’s bearer instrument property, its defining institutional feature, treats self-custody as the operational expression of that property (Antonopoulos, 2015; Böhme et al., 2015; Rudd, 2025b). In the sovereignty-first worldview, opposition to credit leverage and concentrated custody function as social norms [20], making V = 1 and C = 1 configurations inadmissible regardless of operational stability. The sovereignty-first admissible subspace is thus only the 16 configurations where both V = 0 and C = 0 hold. All 16 are stable under the matrix’s stability rule, yet operational stability is not the criterion that produces the restriction. The criterion, I suggest, is the preservation of Bitcoin’s institutional anchor developed in Chapter 7.

The asymmetry is not a difference in how each orientation positions itself within the configuration space. It is a difference in the operation each performs on that space: stability-first optimizes within the entire space using decision criteria supplied by the institutional environment, while sovereignty-first restricts the space using value commitments held independently of that environment. The framework cannot adjudicate between those operations because they occur at the epistemic level the structural model takes as given.

The value filter clarifies the pre-structural restriction. At the epistemic level, broad commitments are translated into political- and implementation-level rules (see Chapter 3). Sovereignty-first applies that filter by excluding configurations before operational rules are constructed for them. The anchor stock rationale is temporal: Bitcoin’s commitment device function depends on institutional commitments that hold against compressive pressure, and those commitments are preserved in the V = 0 and C = 0 region of the configuration space. Configurations outside that region may be operationally stable in the short run but they do not preserve the architecture’s anchor function across time. The sovereignty-first restriction is institutionally rational on time preference grounds (see Chapter 7), not just internally coherent as a worldview.

Bitcoin communities have sustained sovereignty-first restrictions against financialization pressure across the asset’s institutional history (Antonopoulos, 2015; Ammous, 2018; Brunton, 2019; Humayun, 2019). Persistent self-custody norms, opposition to leverage products, and resistance to concentrated custodial arrangements are durable institutional features. Financialization remains the dominant institutional dynamic, while the sovereignty-first restriction continues to hold within communities occupying Bitcoin’s most structurally exposed positions. The configuration space shows where both operations occur. The institutional question is what is at stake when financialization selects a space that sovereignty-first commitments would restrict.

Anchor-stock resilience

Compressive pressure

The cleavage matrix’s analytical content becomes clearest when read against the algorithmic velocity to institutional latency relationship (see Chapter 2). Algorithmic velocity is rising across the institutional environment in which Bitcoin is held, traded, regulated, and contested. Generative AI systems increase the production of analyses, options, and recommendations faster than governance institutions can deliberate over them (Marchant et al., 2011; Taeihagh, 2025). Algorithmic content environments compress attention horizons by selecting and ordering information at platform speed (Wu and Huberman, 2007; Bakshy et al., 2015; Ciampaglia et al., 2015). Financial markets operate on memory horizons within which historical reference events decay quickly (Walsh and Ungson, 1991; Veldkamp, 2011). These pressures increase informational turnover across the substrate within which Bitcoin acquires institutional meaning

Institutional latency rises because the governance forms required to manage increasing informational turnover are slow-moving by design. Regulatory rule-making operates on multi-year cycles; judicial precedent develops over decades; legislative coordination across jurisdictions can take generations. The financialization stack on which stability-first arrangements depend, including fiduciary frameworks (Frankel, 2010), custodial regulations (Awrey, 2020), prudential supervision, clearing arrangements, and crisis-liquidity institutions (Goodhart, 1988; Brunnermeier and Pedersen, 2009), was built for lower informational turnover than algorithmic systems now generate (Chapter 7). The stack does not fail immediately. Its absorption capacity erodes as informational turnover rises against governance response capacity that cannot rise to match it. The cascade pathway is the limit case of this erosion; the exhausted buffer pathway is its frontier.

Long-horizon deliberation for effective governance requires anchor stocks, durable reference points whose temporal dynamics are independent of the informational substrate within which deliberation occurs (Kahneman and Tversky, 1979; North, 1990). Biophysical reference systems (Pauly, 1995), institutional commitment devices (Elster, 2000; Eichengreen, 2019), and historical reference infrastructure (Nora, 1989; Bourdieu and Passeron, 2000) supply that temporal scaffolding through different stock dynamics (see Chapter 7). Contemporary algorithmic velocity and informational turnover degrade those stocks through memory decay in financial markets, attention compression in algorithmic content environments, AI-driven optionality expansion, and reference-point erosion as institutional commitments lose binding force.

Bitcoin as commitment device

Under sovereignty-first commitments, Bitcoin operates as an institutional commitment device, an anchor stock supplying temporal scaffolding where compressive pressures concentrate. Its defining properties (Nakamoto, 2008; Narayanan et al., 2016; De Filippi and Wright, 2018) are commitment properties: fixed supply has binding force that is algorithmic rather than political; settlement finality does not depend on intermediary attestation; bearer instrument property does not require institutional ratification; participation and exit costs are set by protocol rules rather than counterparty relationships. The architecture’s resistance to discretionary revision is the source of its temporal scaffolding capacity.

The commitments associated with self-custody, fixed supply, and independent node operation are more than ideological positions. Read through the time preference lens (Leijonhufvud, 1995; Becker and Mulligan, 1997), they are institutional investments in maintaining a commitment device whose social function is the supply of expansive temporal infrastructure. The longer the commitments hold, the more durable the anchor it supplies; the more durable the anchor, the more the institutional environment can sustain long-horizon deliberation against compressive pressure.

Financialization and anchor loss

Financialization operates against this function by converting Bitcoin from an anchor stock into a conventional financial instrument embedded in high-turnover institutions. ETF wrappers subject the asset to mark-to-market discipline at institutional valuation speed, and custodial concentration shifts the operative property right from algorithmic settlement to intermediary attestation. Derivative markets update the informational substrate at margin system speed. Compliance frameworks and fiduciary precedent integrate the asset into governance arrangements built for instruments whose informational turnover already operates on faster horizons than Bitcoin’s commitment properties can accommodate without erosion.

Operational stability does not by itself settle whether a configuration preserves the commitment device function. That question turns on cleavage values. V = 1 subjects Bitcoin to a high informational turnover environment that erodes anchor stock function regardless of operational stability. C = 1 activates the fundamental transformation (Williamson, 1985) dynamics that compromise Bitcoin’s bearer instrument property regardless of the attestation infrastructure layered over concentrated custody. The commitment device function is preserved in the V = 0 and C = 0 region of the configuration space, the same region sovereignty-first commitments take as admissible (Figure 8.2).

Figure 8.2. The sovereignty-first admissible subspace. Admissibility turns on concentration and leverage alone: the 16 configurations with C = 0 and V = 0 are admissible, while the remaining 48 - which are all available to stability-first - are excluded on principle regardless of the other four cleavages and regardless of operational stability

The cascade pathway is the limit case of stability-first selection because configurations that combine Bitcoin’s architectural commitment properties with the increasing algorithmic velocity financialization imposes generate institutional latency that the available governance system cannot absorb. The lock-in pattern is related: configurations that transfer anchor stock function from the architecture to supporting institutional infrastructure become brittle when hostile policy withdraws or attacks that infrastructure.

Sustaining long-horizon deliberation requires joint investment across anchor types (Chapter 7) because escape from a high-time-preference trap is bounded by the weakest stock. Bitcoin’s commitment device function belongs to the institutional anchor category and its contribution depends on whether institutional dynamics preserve the architecture’s commitment properties. If financialization continues without gateway migration operating at scale or structural unwinding changing the cost-benefit calculus, the institutional anchor category loses one of its relatively few potentially durable contemporary candidates just as compressive pressure intensifies across biophysical and historical anchors as well.

Resilience as institutional value

Bitcoin's sovereignty-first position is often defended on normative grounds: bearer instrument property as the value the architecture instantiates; exit options as a check against governance overreach; and individual key custody as a hedge against jurisdictional failure. The institutional economics reading goes further. Sovereignty-first configurations preserve Bitcoin's anchor stock function, and that function gives the asset a capacity to counteract the compressive pressure generated by rising algorithmic velocity and informational turnover.

Bitcoin's temporal architecture – block production, the difficulty adjustment, the halving schedule, the 21-million supply cap, and a governance form that resists takeover and dampens epistemic-level shifts in core commitments – supplies expansive temporal scaffolding. Whether contemporary institutional dynamics sustain the configurations in which low time preferences dominate remains an empirical question. Linking temporal anchoring to time preferences makes it testable, distinguishing whether low time preferences are an effect of Bitcoin exposure or whether adoption instead reveals the prior preferences of actors who already highly value the future. Either reading leaves the analytical stakes intact: Bitcoin either remains a sovereignty-first commitment device within a compressive institutional environment or it becomes just one more financial instrument operating inside that environment.

The anchor stock function has a public-good-like dimension (Samuelson, 1954). Bitcoin's market price records private willingness to hold exposure to the asset but it does not capture the full institutional value of a credible, non-discretionary commitment device. That value accrues beyond the holders who pay for it: a live reference point standing against elastic-credit governance helps sustain long-horizon orientation under compressive pressure, and the benefit reaches participants in the wider monetary and institutional environment whether or not they hold the asset. A benefit of this kind, conferred outside the price mechanism and not rival in consumption, is a positive externality (Coase, 1960; Cornes and Sandler, 1996). Its magnitude may be hard to measure but the difficulty of quantification does not make the benefit institutionally irrelevant. Bitcoin's institutional value may therefore exceed its market value. That excess goes unpriced and the anchor function that produces it is preserved in the same V = 0 and C = 0 region that sovereignty-first commitments hold admissible.

Conclusion

Six cleavages generate 64 configurations whose stability follows from how structural conditions interact rather than from any single variable. Credit leverage is the primary divider. Where leverage is present, credible attestation forces informational turnover that the available governance forms cannot absorb, while opacity routes the same dynamics through intermediary buffering wherever absorption capacity exists. A narrower brittleness appears under hostile policy, where concentrated and transparent custody turns the legibility of intermediary positions into a liability. These are distinct governance problems occupying distinct regions of the space, not symmetric variants of one logic.

Operational durability and epistemic admissibility are different criteria. Stability-first commitments select within the full configuration space on profitability, transaction cost, and institutional integration, ranking configurations without excluding any. Sovereignty-first commitments restrict the space in advance to the region where V = 0 and C = 0, because the excluded configurations surrender the commitment properties that make Bitcoin institutionally distinctive even when they remain operationally stable. Every configuration in that admissible region is stable but stability is not the criterion the restriction tracks; at its core, it tracks the preservation of Bitcoin’s anchor stock function.

Financialization carries institutional momentum because its supporting infrastructure – custody relationships, compliance investments, fiduciary precedent, ETF wrappers, derivative markets, and regulatory routine – generates increasing returns (Arthur, 1989) that progressively narrow the feasible set. Bitcoin does not face a choice between purity and contact with the financial system, since it already interacts with that system through several governance forms at once. What divides those interactions is whether they preserve Bitcoin’s commitment properties or convert them into ordinary financial exposure. Stability-first integration can hold operational durability while moving Bitcoin toward configurations that no longer carry the same institutional meaning, whereas sovereignty-first commitments preserve that meaning only through continuous maintenance the surrounding environment does not reward.

The stakes are temporal. Bitcoin’s commitment properties supply an anchor stock – a reference point whose binding force is algorithmic rather than political – at the moment when rising algorithmic velocity and informational turnover are eroding the biophysical, institutional, and historical stocks on which long-horizon deliberation depends (Chapter 7). The cascade pathway is the limit case of that erosion and the lock-in pattern its frontier, each arising where governance form requirements outrun governance form availability. A credible non-discretionary commitment device supplies temporal scaffolding beyond its holders, a value only partly captured in Bitcoin’s market price. Whether that scaffolding survives is not settled by operational stability but by which configurations the institutional environment selects; left to its own momentum, financialization selects against the region where the anchor stock function would otherwise hold.

References

Acemoglu, D 2025. The simple macroeconomics of AI. Economic Policy 40: 13-58. https://doi.org/10.1093/epolic/eiae042

Akerlof, GA 1970. The market for "lemons": quality uncertainty and the market mechanism. The Quarterly Journal of Economics 84: 488-500. https://doi.org/10.2307/1879431

Ammous, S 2018. The Bitcoin Standard: The Decentralized Alternative to Central Banking. Hoboken, New Jersey: Wiley.

Antonopoulos, AM 2015. Mastering Bitcoin: Unlocking Digital Cryptocurrencies. Sebastol, CA: O'Reilly Media, Inc.

Arthur, WB 1989. Competing technologies, increasing returns, and lock-in by historical events. The Economic Journal 99: 116-131. https://doi.org/10.2307/2234208

Awrey, D 2020. Bad money. Cornell Law Review 106: 1-90. https://publications.lawschool.cornell.edu/lawreview/wp-content/uploads/sites/2/2021/02/Dan-Awrey-Bad-Money.pdf

Ba, H-L and ÖF Şen 2024. Explaining variation in national cryptocurrency regulation: implications for the global political economy. Review of International Political Economy 31: 1472-1495. https://doi.org/10.1080/09692290.2024.2325403

Bakshy, E, S Messing and LA Adamic 2015. Exposure to ideologically diverse news and opinion on Facebook. Science 348: 1130-1132. https://www.science.org/doi/abs/10.1126/science.aaa1160

Becker, GS and CB Mulligan 1997. The endogenous determination of time preference. The Quarterly Journal of Economics 112: 729-758. https://doi.org/10.1162/003355397555334

Benson, V, B Adamyk, A Chinnaswamy, et al. 2024. Harmonising cryptocurrency regulation in Europe: opportunities for preventing illicit transactions. European Journal of Law and Economics 57: 37-61. https://doi.org/10.1007/s10657-024-09797-w

Boettke, PJ, CJ Coyne and P Newman 2016. The history of a tradition: Austrian economics from 1871 to 2016. In Research in the History of Economic Thought and Methodology Vol. 34A, eds. L Fiorito, S Scheall and CE Suprinyak, 199-243. Bingley, UK: Emerald Group Publishing Limited. https://doi.org/10.1108/S0743-41542016000034A007

Böhme, R, N Christin, B Edelman, et al. 2015. Bitcoin: economics, technology, and governance. Journal of Economic Perspectives 29: 213-238. http://dx.doi.org/10.1257/jep.29.2.213

Bourdieu, P and J-C Passeron 2000. Reproduction in Education, Society and Culture, Second Edition. London: Sage.

Brunnermeier, MK, A Crockett, CAE Goodhart, et al. 2009. The fundamental principles of financial regulation. Geneva Reports on the World Economy 11, https://cepr.org/publications/books-and-reports/geneva-11-fundamental-principles-financial-regulation

Brunnermeier, MK and LH Pedersen 2009. Market liquidity and funding liquidity. The Review of Financial Studies 22: 2201-2238. https://doi.org/10.1093/rfs/hhn098

Brunton, F 2019. Digital Cash: The Unknown History of the Anarchists, Utopians, and Technologists Who Created Cryptocurrency. Princeton, N.J.: Princeton University Press.

Caldara, D and M Iacoviello 2022. Measuring geopolitical risk. American Economic Review 112: 1194–1225. https://doi.org/10.1257/aer.20191823

CFTC and SEC 2026. Application of the Federal Securities Laws to certain types of crypto assets and certain transactions involving crypto assets. Federal Register 81: 13714-13733. https://www.govinfo.gov/content/pkg/FR-2026-03-23/pdf/2026-05635.pdf

Ciampaglia, GL, A Flammini and F Menczer 2015. The production of information in the attention economy. Scientific Reports 5: 9452. https://doi.org/10.1038/srep09452

Coase, RH 1960. The problem of social cost. The Journal of Law and Economics 3: 1. https://doi.org/10.1086/466560

Coase, RH 1992. The institutional structure of production. The American Economic Review 82: 713-719. http://www.jstor.org/stable/2117340

Cornes, R and T Sandler 1996. The Theory of Externalities, Public Goods, and Club Goods, 2nd Edition. Cambridge, U.K.: Cambridge University Press.

Dang, TV, G Gorton, B Holmström, et al. 2017. Banks as secret keepers. The American Economic Review 107: 1005-1029. http://www.jstor.org/stable/44251585

De Filippi, P and B Loveluck 2016. The invisible politics of Bitcoin: governance crisis of a decentralised infrastructure. Internet Policy Review 5. https://doi.org/10.14763/2016.3.427

De Filippi, P and A Wright 2018. Blockchain and the Law: The Rule of Code. Cambridge MA: Harvard University Press.

Duffie, D and H Zhu 2011. Does a central clearing counterparty reduce counterparty risk? The Review of Asset Pricing Studies 1: 74-95. https://doi.org/10.1093/rapstu/rar001

Eichengreen, B 2019. Globalizing Capital: A History of the International Monetary System, Third Edition. Princeton, NJ: Princeton University Press.

Elster, J 2000. Ulysses Unbound: Studies in Rationality, Precommitment, and Constraints. Cambridge: Cambridge University Press.

Frankel, TT 2010. Fiduciary Law. Oxford, U.K.: Oxford University Press.

Geanakoplos, J 2010. The leverage cycle. NBER Macroeconomics Annual 24: 1-66. https://doi.org/10.1086/648285

Goodhart, CAE 1988. The Evolution of Central Banks. Cambridge, MA: MIT Press.

Hatzius, J, J Briggs, D Kodnani, et al. 2023. The potentially large effects of Artificial Intelligence on economic growth. Goldman Sachs Global Investment research report, https://www.gspublishing.com/content/research/en/reports/2023/03/27/d64e052b-0f6e-45d7-967b-d7be35fabd16.html

Hayes, A 2019. The socio-technological lives of Bitcoin. Theory, Culture & Society 36: 49-72. https://doi.org/10.1177/0263276419826218

Hirschman, AO 1970. Exit, Voice, and Loyalty: Responses to Decline in Firms, Organizations, and States. Cambridge, MA: Harvard University Press.

Hodgson, GM 1998. The approach of Institutional Economics. Journal of Economic Literature 36: 166-192. https://www.jstor.org/stable/2564954

Humayun, SM 2019. Creation and resilience of decentralized brands: Bitcoin & the blockchain. PhD dissertation, Schulich School of Business, York University, Toronto, https://yorkspace.library.yorku.ca/xmlui/handle/10315/37662

Iacoviello, M, D Caldara, M Penn, et al. 2024. Do geopolitical risks raise or lower inflation? SSRN preprint, http://dx.doi.org/10.2139/ssrn.4852461

IMF 2026. Fiscal Monitor: Fiscal Policy under Pressure: High Debt, Rising Risks. Washington, DC: International Monetary Fund (IMF).

Kahneman, D and A Tversky 1979. Prospect theory: an analysis of decision under risk. Econometrica 47: 263-291. https://doi.org/10.2307/1914185

Keynes, JM 1930. A Treatise on Money. London: Macmillan.

Lavoie, M 2014. Post-Keynesian Economics: New Foundations. Cheltenham, UK: Edward Elgar.

Leijonhufvud, A 1995. Adaptive behavior, market processes and the computable approach. Revue économique 46: 1497-1510.

Marchant, GE, BR Allenby and JR Herkert (eds). 2011. The Growing Gap Between Emerging Technologies and Legal-Ethical Oversight: The Pacing Problem. Dordrecht: Springer

Maurer, B, TC Nelms and L Swartz 2013. “When perhaps the real problem is money itself!”: the practical materiality of Bitcoin. Social Semiotics 23: 261-277. https://doi.org/10.1080/10350330.2013.777594

Minsky, HP 1986. Stabilizing an Unstable Economy. New York: Neuaufl.

Nabben, K 2023. Cryptoeconomics as governance: an intellectual history from “Crypto Anarchy” to “Cryptoeconomics”. Internet Histories 7: 254–276. https://doi.org/10.1080/24701475.2023.2183643

Nakamoto, S 2008. Bitcoin: a peer-to-peer electronic cash system. Unpublished white paper, https://bitcoin.org/bitcoin.pdf

Narayanan, A, J Bonneau, E Felten, et al. 2016. Bitcoin and Cryptocurrency Technologies. Princeton, New Jersey: Princeton University Press.

Nora, P 1989. Between memory and history: les lieux de mémoire. Representations: 7-24. https://doi.org/10.2307/2928520

North, DC 1990. Institutions, Institutional Change and Economic Performance. Cambridge MA: Cambridge University Press.

Notland, JS, M Nowostawski and J Li 2025. An empirical study on governance in Bitcoin’s consensus evolution. ACM Transactions on Software Engineering and Methodology 34: 63. https://doi.org/10.1145/3699600

Ostrom, E 1990. Governing the Commons: The Evolution of Collective Action. Cambridge, UK: Cambridge University Press.

Ostrom, E 2010. Beyond markets and states: polycentric governance of complex economic systems. The American Economic Review 100: 641-672. http://www.jstor.org/stable/27871226

Ostrom, V 1997. The Meaning of Democracy and the Vulnerability of Democracies: A Response to Tocqueville's Challenge. Ann Arbor: University of Michigan Press.

Pauly, D 1995. Anecdotes and the shifting baseline syndrome of fisheries. Trends in Ecology and Evolution 10: 430. https://doi.org/10.1016/s0169-5347(00)89171-5

Ritchey, T 2011. Wicked Problems – Social Messes. Decision Support Modelling with Morphological Analysis. Berlin: Springer.

Rothbard, MN 1977. Praxeology: the methodology of Austrian Economics. In Foundations of Modern Austrian Economics, ed. E Dolan, 19-39. Kansas City: Sheed and Ward. https://mises.org/mises-daily/praxeology-methodology-austrian-economics

Rudd, MA 2023. Bitcoin is full of surprises. Challenges 14: 27. https://doi.org/10.3390/challe14020027

Rudd, MA 2024. 40 questions for shaping a policy-salient Bitcoin research agenda. SSRN preprint, https://dx.doi.org/10.2139/ssrn.4821335

Rudd, MA 2025a. Important Bitcoin information gaps and research needs for 2024. SSRN preprint, https://dx.doi.org/10.2139/ssrn.5146515

Rudd, MA 2025b. A Bitcoin research agenda: 100 critical information gaps for policy and practice, 2024 edition. SSRN preprint, http://dx.doi.org/10.2139/ssrn.5359261

Rudd, MA and D Porter 2025. Bitcoin supply, demand, and price dynamics. Journal of Risk and Financial Management 18: 570. https://doi.org/10.3390/jrfm18100570

Rudd, MA 2026. Bitcoin research priorities in 2025: beyond first-order effects. SSRN preprint, https://dx.doi.org/10.2139/ssrn.6032217

Samuelson, PA 1954. The pure theory of public expenditure. The Review of Economics and Statistics 36: 387-389. https://doi.org/10.2307/1925895

Sargent, TJ and N Wallace 1981. Some unpleasant monetarist arithmetic. Federal reserve bank of minneapolis quarterly review 5: 1-17. https://link.springer.com/chapter/10.1007/978-1-349-06284-3_2

Swartz, L 2018. What was Bitcoin, what will it be? The techno-economic imaginaries of a new money technology. Cultural Studies 32: 623-650. https://doi.org/10.1080/09502386.2017.1416420

Taeihagh, A 2025. Governance of generative AI. Policy and Society 44: 1-22. https://doi.org/10.1093/polsoc/puaf001

Veblen, T 1898. Why is economics not an evolutionary science? The Quarterly Journal of Economics 12: 373-397. https://doi.org/10.2307/1882952

Veldkamp, LL 2011. Information Choice in Macroeconomics and Finance. Princeton, NJ: Princeton University Press.

Von Hayek, FA 2009. Denationalisation of Money, Third Edition. Auburn, Alabama: Ludwig von Mises Institute.

Walsh, JP and GR Ungson 1991. Organizational memory. The Academy of Management Review 16: 57-91. https://doi.org/10.2307/258607

Williamson, OE 1985. The Economic Institutions of Capitalism. New York: The Free Press.

Williamson, OE 1991. Comparative economic organization: the analysis of discrete structural alternatives. Administrative Science Quarterly 36: 269-296. https://doi.org/10.2307/2393356

Williamson, OE 2000. The New Institutional Economics: taking stock, looking ahead. Journal of Economic Literature 38: 595-613. https://doi.org/10.2307/2565421

Wu, F and BA Huberman 2007. Novelty and collective attention. Proceedings of the National Academy of Sciences 104: 17599-17601. https://doi.org/10.1073/pnas.0704916104

Zwicky, F 1967. The morphological approach to discovery, invention, research and construction. In New Methods of Thought and Procedure, eds. F Zwicky and AG Wilson, 273-297. Berlin, Heidelberg: Springer Berlin Heidelberg. https://doi.org/10.1007/978-3-642-87617-2_14

Comments ()